SAFE vs BSA Air: The Definitive Guide for Entrepreneurs and Investors

Everyone in the startup ecosystem has heard of Y Combinator's SAFE and the French BSA Air. Many talk about them, but too many still get burned. Here's the comprehensive guide to understanding these early-stage financing instruments that could save your cap table.

1. The Fundamentals: Why These Instruments Exist

Early-stage startup financing has always presented a major challenge: how do you invest in a company that's too young to be properly valued? Historically, two approaches dominated:

Equity round: Complete valuation, heavy legal documentation, complex negotiations

Convertible notes: Convertible loans with maturity dates and interest, creating debt on the balance sheet

Both mechanisms presented significant drawbacks for nascent companies. It's in this context that SAFE and BSA Air were born.

2. The SAFE Dissected: Mechanisms and Evolutions

2.1 Anatomy of a SAFE (Simple Agreement for Future Equity)

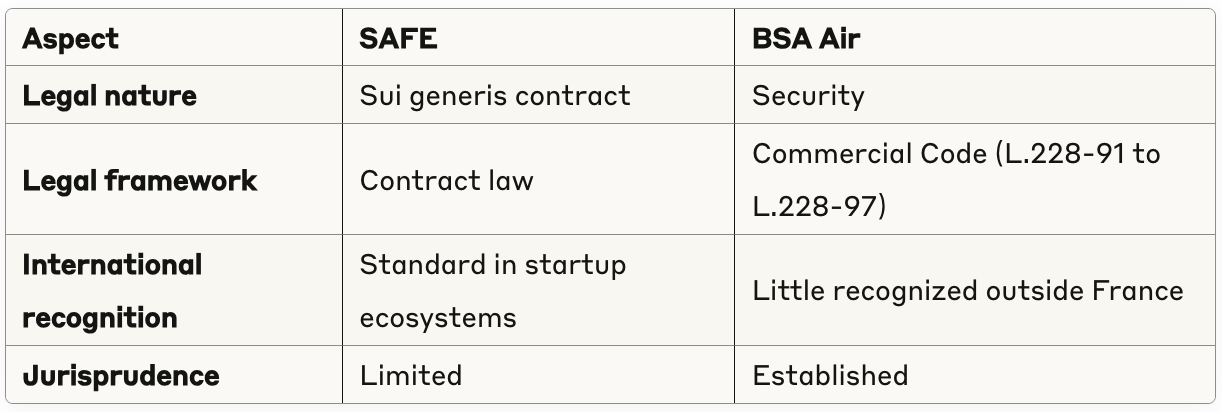

Created by Y Combinator in 2013, the SAFE is a convertible investment contract that is neither debt nor equity. Its fundamental characteristics:

No maturity date: Unlike convertible notes, no conversion deadline

No interest: The investor doesn't accumulate interest on their investment

Automatic conversion: Upon a qualified equity round (typically defined by a minimum amount)

The key terms negotiated in a SAFE are:

Valuation cap: Maximum valuation ceiling for conversion

Discount: Reduction applied relative to new investors (typically 10-25%)

MFN clause (Most Favored Nation): Guarantee to obtain the best future terms

2.2 The Critical Evolution: Pre-Money vs Post-Money SAFE

In 2018, Y Combinator introduced a major modification that changed the game: the Post-Money SAFE.

Pre-Money SAFE (original):

Cap is defined as a pre-money valuation

Dilution related to the SAFE itself and other SAFEs isn't calculated in advance

Calculation formula:

Shares = Investment amount / (Pre-money valuation / Existing shares)Post-Money SAFE (2018+):

Cap is defined as a post-money valuation

Dilution is clearly defined from the start

Calculation formula:

Shares = (Investment amount / Cap) × Total shares after dilutionThis transition seemed to bring more clarity, but it introduced a hidden complexity: the cumulative effect of consecutive SAFEs.

2.3 The Case Study: The Cumulative Effect of Post-Money SAFEs

Let's take a concrete example to illustrate this often-ignored issue:

You're the CEO and hold 1,000,000 shares. You raise three consecutive SAFEs:

At first glance, these SAFEs seem equivalent: each represents a 10% dilution regardless of the calculation method.

But here's where the devil hides in the details:

Scenario 1 - All your SAFEs are Pre-Money cap:

For each SAFE, you calculate an ownership percentage of 10%, or 111,111 new shares per SAFE.

New shares = (Existing shares / (1 - Dilution)) - Existing shares

New shares = (1,000,000 / 0.9) - 1,000,000 = 111,111Total after three SAFEs: 333,333 new shares Your final ownership: 1,000,000 / 1,333,333 = 75%

Scenario 2 - All your SAFEs are post-Money cap:

Each SAFE creates a 10% dilution, but on a cumulative basis:

First SAFE: 10% = 111,111 new shares

Second SAFE: 10% of (1,000,000 + 111,111) = 123,457 new shares

Third SAFE: 10% of (1,000,000 + 111,111 + 123,457) = 137,174 new sharesTotal after three SAFEs: 371,742 new shares Your final ownership: 1,000,000 / 1,371,742 = 72.9%

The difference intensifies with the amount raised and the number of SAFEs. In a more extreme scenario, with SAFEs at different conditions, the impact can be far more dramatic.

After an additional equity round of $8M at $40M post-money (20% dilution), your ownership would go to:

Pre-Money Scenario: 75% × 0.8 = 60%

Post-Money Scenario: 72.9% × 0.8 = 58.3%

To precisely simulate these effects, Carta offers a free tool

3. The BSA Air: The French Alternative Explained

3.1 What is a BSA Air?

The BSA Air (Bon de Souscription d'Actions) is the French adaptation designed to address the same needs as the SAFE, but within the French legal framework. Unlike the SAFE, the BSA Air is a security governed by the French Commercial Code.

Fundamental structure:

Warrant: Gives the right to purchase shares at a predetermined price

Subscription price: Generally symbolic (€1)

Exercise price: Actual amount invested, paid upon conversion

Exercise conditions: Events triggering conversion (fundraising, sale...)

Validity period: Unlike the SAFE, the BSA has a limited duration (typically 5-10 years)

3.2 Tax Benefits: The BSA Air's Major Asset

The main advantage of the BSA Air for French investors lies in its optimized tax treatment:

IR-PME tax reduction: Investments via BSA Air may be eligible for income tax reduction for SME investment (18% of the amount invested, capped)

Capital gains tax regime: Advantageous tax treatment when selling the shares obtained

Flat tax: Application of the 30% flat tax on capital gains

To be eligible for these benefits, the structuring must be precise and comply with the conditions set by the tax authorities.

4. Detailed Comparative Analysis: SAFE vs BSA Air

4.1 Legal Framework and Recognition

4.2 Process and Costs

4.3 Flexibility and Structure

4.4 Tax and Accounting Implications

5. Practical Guide: When and How to Use Each Instrument

5.1 Optimal Scenarios for SAFE

The SAFE is particularly suitable in the following contexts:

Ideal company profile:

Startups with immediate international ambitions

Business models requiring rapid iterations and potential pivots

Rapid funding cycles before Series A

B2C or deep tech companies with uncertain revenue models

Ideal investor profile:

International angels and VCs

Investors familiar with the American startup ecosystem

Seed funds with international experience

Optimal structure:

Reasonable cap (generally 4-8× the amount invested)

Moderate discount (15-20%)

Well-formulated MFN clause

Bilingual documentation

5.2 Optimal Scenarios for BSA Air

The BSA Air is particularly relevant in the following situations:

Ideal company profile:

French startups without immediate international ambitions

Relatively predictable business models

Companies with tangible assets or established intellectual property

B2B companies with identifiable commercial pipeline

Ideal investor profile:

Tax-sensitive French business angels

French family offices and corporate ventures

French institutional investors

Optimal structure:

Symbolic subscription price (€1)

Exercise price corresponding to the investment

Well-defined exercise conditions

Balanced anti-dilution protection

5.3 The Hybrid Strategy: The Best of Both Worlds

In many cases, a hybrid approach can offer maximum flexibility:

Strategy 1: Segregation by investor type

SAFE for international investors

BSA Air for French investors

Strategy 2: Mirror documentation

Creation of equivalent documents in both formats

Identical economic terms with adapted legal structures

Systematic bilingual documentation

Strategy 3: Coordinated early conversion

Upstream planning for conversion of both types of instruments

Alignment of conversion conditions

Unified preferred share structure

6. Critical Errors to Avoid and Solutions

6.1 SAFE Pitfalls

Error #1: SAFE without cap

Problem: Potentially unlimited dilution

Solution: Always insist on a reasonable cap

Error #2: Multiplication of Post-Money SAFEs without modeling

Problem: Underestimated cumulative dilution effect

Solution: Precisely model each scenario with specialized tools

Error #3: SAFEs with different terms without hierarchization

Problem: Potential conflicts during conversion

Solution: Clearly structure conversion priority

Error #4: Incomplete documentation for conversion

Problem: Disputes over interpretation during the next round

Solution: Precisely define conversion mechanisms, including for alternative scenarios

6.2 BSA Air Pitfalls

Error #1: Non-compliant structure for tax advantage

Problem: Loss of expected tax benefits

Solution: Validation by a specialized tax expert

Error #2: Inappropriate validity period

Problem: Premature expiration before conversion

Solution: Calibrate duration according to business plan (minimum 5-7 years)

Error #3: Overly restrictive exercise conditions

Problem: Impossible conversion in certain scenarios

Solution: Provide alternative exercise clauses

Error #4: Non-anticipation of international constraints

Problem: Incompatibility with future investors

Solution: Provide mechanisms for conversion into standard international instruments

7. Practical Checklist and Resources

7.1 Checklist for Founders

Before signing a SAFE:

✅ Model the dilutive impact on your cap table (pre and post-conversion)

✅ Analyze the cumulative effect of all existing and planned SAFEs

✅ Check compatibility with your jurisdiction and corporate structure

✅ Prepare advance conversion documentation

✅ Anticipate questions from future institutional investors

Before signing a BSA Air:

✅ Verify that your company's bylaws allow for issuance

✅ Consult an expert on tax and accounting implications

✅ Prepare the complete timeline for legal procedures

✅ Anticipate anti-dilution protection mechanisms

✅ Plan for alternative exercise scenarios

7.2 Checklist for Investors

Before investing via SAFE:

✅ Calculate your ownership percentage in different fundraising scenarios

✅ Check other SAFEs already issued and their conditions

✅ Analyze protection mechanisms in case of liquidity or down-round

✅ Understand potential limitations on your governance rights

✅ Plan your strategy for future rounds

Before investing via BSA Air:

✅ Check your eligibility for tax benefits (especially IR-PME)

✅ Analyze the issuance contract in detail, particularly exercise conditions

✅ Understand adjustment and anti-dilution mechanisms

✅ Check validity period in relation to the business plan

✅ Plan exit scenarios and potential liquidity

7.3 Essential Resources

For SAFE:

For BSA Air:

Conclusion: Beyond the Instruments

Technical complexity shouldn't obscure the essential: these instruments are merely vehicles serving a founder-investor relationship that extends over time.

The choice between SAFE and BSA Air, or their clever combination, should reflect:

The company's strategic vision

Compatibility with current and future investors

Balance between execution simplicity and legal protection

Tax and accounting optimization according to relevant jurisdictions

In the end, transparency and alignment of interests remain the most determining factors for successful early-stage financing.

As the sector adage aptly reminds us: "STAY SAFE ;-)" - but above all, stay informed and aware of the implications of each of your financing decisions.

If this article was useful to you, share it with a founder or investor who might need it. And if you want to discuss your particular case, don't hesitate to contact me directly.

Previous articles you'll love :

Catch you soon!

👏👏👏

Thanks for this guide!